Fixed Mortgage Ending in 2026? Review Your UK Remortgage Options Early

Fixed Your Mortgage in 2021? Your Deal May Be Ending Soon

If you secured a fixed-rate mortgage in 2021, your deal is likely expiring in 2026.

With thousands of UK homeowners coming off 2-, 3- and 5-year fixed mortgages, this year represents a major remortgage milestone. What you do next could significantly affect your monthly repayments and long-term mortgage costs.

Before your mortgage automatically moves onto your lender’s Standard Variable Rate (SVR), it’s important to review your options.

A structured mortgage review can help you understand where you stand — calmly and without pressure.

UK Mortgage Rates in 2026: What’s Changed Since 2021?

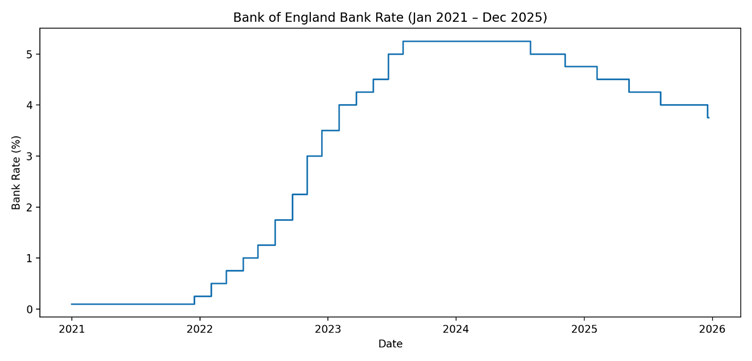

In 2021:

- The Bank of England base rate was 0.1%

- Fixed mortgage rates were at historic lows

In 2023:

- The base rate peaked at 5.25%

- Many borrowers experienced payment increases

By late 2025:

- The base rate was reduced to 3.75%

- Lender competition increased

- Mortgage pricing began stabilising

While rates are not back to 2021 levels, the mortgage market in 2026 is more settled compared to the volatility seen in recent years.

Mortgage pricing reflects funding markets and expectations, not just the base rate alone, which is why reviewing your position now can be valuable.

What Happens When Your Fixed Rate Ends?

When your fixed mortgage expires, it usually moves onto your lender’s Standard Variable Rate (SVR).

An SVR:

- Is set by your lender

- Can increase or decrease

- Is often higher than fixed or tracker products

For borrowers who fixed at very low rates in 2021, the change can be noticeable.

Reviewing your options before expiry helps avoid drifting onto a potentially higher rate unintentionally.

Remortgage or Product Transfer in 2026?

When your deal ends, you generally have two options:

Product Transfer

Switch to a new deal with your current lender.

- Typically quicker

- Often fewer checks required

- Limited to that lender’s available products

Remortgage

Switch to a new lender.

- Access to a wider range of UK mortgage products

- May provide different rates or feature options

- Requires affordability checks and may involve legal work

The most suitable option depends on:

- Loan-to-value (LTV)

- Credit profile

- Income and affordability

- Property value

- Fees and total cost over the fixed period

The headline rate alone does not determine overall value.

When Should You Start Your Remortgage?

Many lenders allow you to secure a new deal up to six months before your current rate ends.

Starting early can:

- Protect you from moving onto SVR

- Provide time to compare options

- Reduce last-minute pressure

- Allow flexibility if market conditions shift

2026 is expected to be a busy remortgage year, so early preparation provides greater control.

30-Minute Mortgage Rate Review

At BVS Mortgages Financial Services Ltd, we offer a structured review designed to give you clarity.

During your review, we:

- Compare product transfer and remortgage options

- Assess overall cost, not just interest rate

- Explain fees, incentives and repayment structure

- Provide straightforward, regulated advice

- Confirm honestly if switching is not suitable

There is no obligation to proceed.

The purpose is simple: ensure you understand your options before your fixed mortgage ends.

Why Choose Us?

- FCA Regulated

We are regulated by the Financial Conduct Authority.

- Wide Lender Access

We compare products from a broad range of UK mortgage lenders.

- Transparent Fees

All costs are explained clearly before you proceed.

- Experienced Advisers

Qualified professionals supporting homeowners across the UK.

- No-Pressure Advice

If switching does not benefit you, we will say so.

Book Your Mortgage Review

If your fixed mortgage is ending in 2026, reviewing early can help you make an informed decision with confidence.

Book your 30-minute mortgage review today.

Important Mortgage Information

Your home may be repossessed if you do not keep up with repayments on your mortgage.

Mortgage approval is subject to status, affordability assessment and lender criteria.

Interest rates and product availability are subject to change.

Not all applicants will qualify for all products. Eligibility depends on individual circumstances.

BVS Mortgages and Financial Services Ltd is an appointed representative of The Openwork Partnership, a trading style of Openwork Limited, authorised and regulated by the Financial Conduct Authority.

Approved by The Openwork Partnership on 09/04/2026.

Published date 15/04/2026